How You’re Protected

Learning that your life or health insurance company is in trouble can be alarming, but policyholders can take comfort in knowing that state guaranty associations are there to provide protection and continuing coverage.

Since NOLHGA was created in 1983, state guaranty associations have provided protection to more than 3.29 million policyholders, guaranteed $30.44 billion in coverage benefits and paid more than $10 billion directly to policyholders.

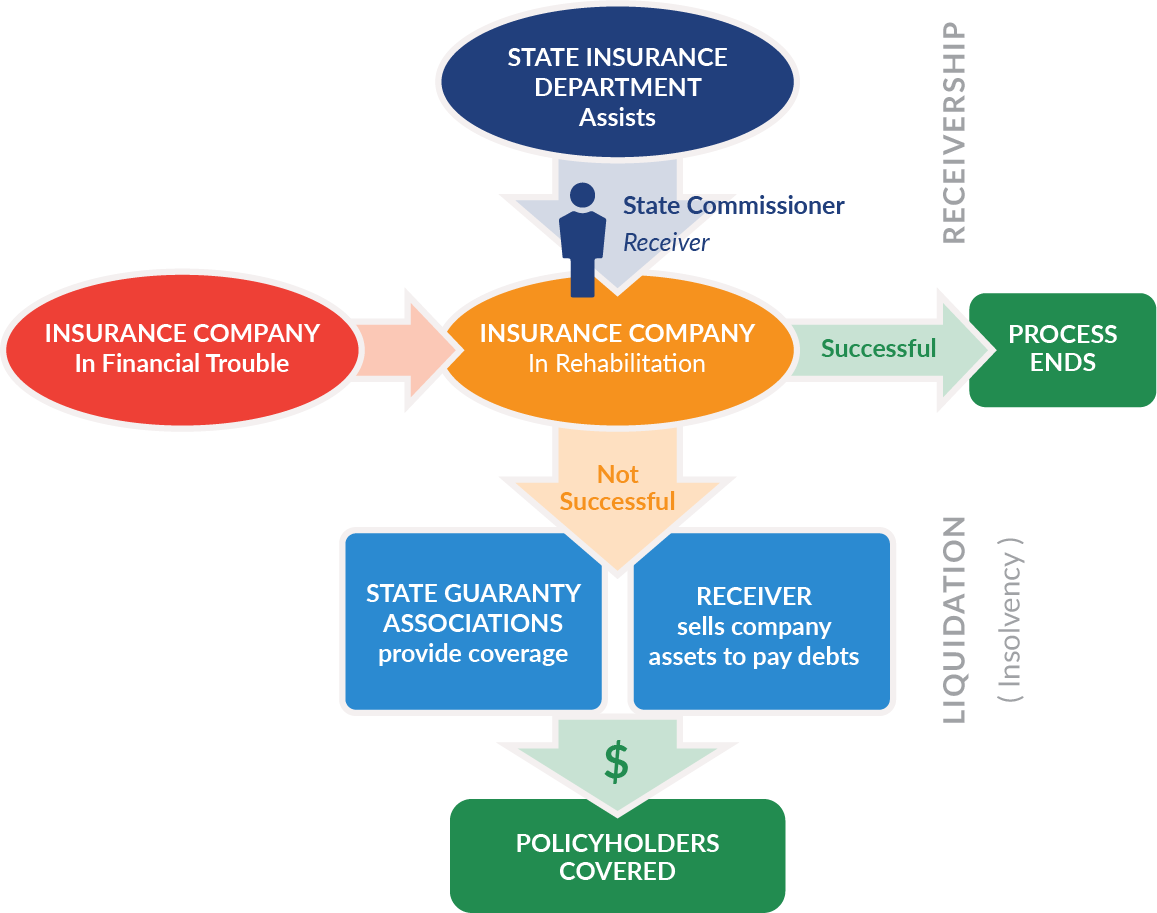

What Happens When an Insurance Company Fails?

Insurance is regulated by the states—each state has an insurance department that oversees the financial stability of companies doing business in that state. When a company experiences financial troubles and can’t meet its obligations to policyholders, the insurance commissioner in the company’s home state (also called the domiciliary state) steps in to help the company try to recover financially.

A receivership is a court proceeding, and the judicial process is governed by the state’s court system. Each state requires that the insurance commissioner be appointed the “Receiver” of the insurer to administer the receivership under court supervision.

In the first stage of receivership, called rehabilitation, the Receiver steps in to help the company try to recover financially. If efforts to rehabilitate the company succeed, the receivership process ends. However, if the company’s financial troubles are too severe to resolve, the Receiver asks a state court for permission to close down the company and sell its assets to pay its debts. This is called liquidation or insolvency, and it’s similar to a company declaring bankruptcy.

It’s important to note that policyholders will always receive 100% of their covered policy benefits up to the guaranty association’s coverage limit (in most states, coverage of more than one policy is subject to an aggregate limit per person). Policies with benefits higher than the guaranty association’s coverage limit may have a claim to receive a share of their benefits from the remaining assets in the liquidated company. Also, the guaranty association in the policyholder’s state of residence at the time the company is ordered into liquidation generally provides coverage, regardless of where the policy was originally purchased.

What Is a Guaranty Association?

Guaranty associations operate in all 50 states, Puerto Rico, and the District of Columbia, and they play a crucial role in safeguarding policyholders when their insurance company goes out of business. Guaranty associations protect policyholders in their state if an insurance company fails (also known as insolvency or liquidation). They don’t sell insurance, but most insurance companies licensed to sell life, health, or annuity policies in a state must be members of that state’s guaranty association.

State life and health insurance guaranty associations were created to do three things:

Continuing Coverage

State guaranty associations step in when an insurance company fails. Their primary goal is to provide continuing coverage for policyholders of the failed insurer. This ensures that even if the original company goes out of business, policyholders still have insurance protection.

Benefit Protection

Guaranty associations also work to protect the benefits due to policyholders. They honor the terms of existing policies (up to the legal limit) and prevent disruptions for those relying on insurance coverage. In more than 40 years, the guaranty associations have never failed to pay a covered claim.

Quick Protection

Guaranty associations collaborate through the National Organization of Life & Health Insurance Guaranty Associations (NOLHGA) to protect policyholders quickly and efficiently. NOLHGA helps coordinate efforts across states when dealing with large-scale challenges caused by national insurance company failures.

How Guaranty Associations Work

Even before an insurance company is liquidated, the guaranty associations usually work with the insurance department and the Receiver on a plan to protect policyholders. Once liquidation is ordered, the plan goes into effect, and the guaranty associations step in to provide coverage for policyholders who are residents of their state. This coverage is provided up to the limits set by state laws.

If the liquidated company lacks sufficient funds to meet its policyholder obligations, each state guaranty association uses a combination of the company’s remaining assets and funds contributed by member insurers in the state (called assessments) to pay claims and continue coverage. These assessments are based on the premiums collected by each insurer in that state for the type of insurance policy in question.

If your policy has benefits above your guaranty association’s limit, that doesn’t mean you lose those benefits. In most states, those amounts become a claim against the estate of the failed insurer, and they may be paid in part by the company’s remaining assets.

Coverage Levels by State

NOTES: This information is general in nature. It is based on information available as of June 1, 2025, and is subject to possible change in the future. It is not intended as legal advice, and no liability is assumed in connection with its use. For specific coverage provisions, consult the applicable guaranty association statutes. NOLHGA believes the information provided on this site is accurate. However, if there is any inconsistency between the Guaranty Association Act or any other law or regulation and the information on this website, the relevant law will control.

The guaranty association laws of some states limit the interest rate on life insurance and annuity contracts that may be covered by the association. The protection is also subject to other applicable limits and exclusions on coverage, including an exclusion for portions of a policy or contract not guaranteed by the insurer or under which the risk is borne by the contract owner.

For annuities, guaranty association coverage levels apply to the present value of annuity benefits. Guaranty association protection generally applies to individual annuity contracts or group annuity certificates that are issued to and owned by an individual or to benefits that the insurer guarantees to an individual under the annuity contract or certificate.

51

Alabama

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Alaska

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Arizona

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Arkansas

$300,000

Life Insurance Death Benefits

$300,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$300,000

Annuities

California

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$668,205

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$668,205

Long-Term Care & Disability Income Insurance Benefits

$668,205

Other Health Insurance Benefits

$250,000

Annuities

Notes

- Life Insurance Death Benefits: California covers 80% of death benefits with a $300,000 benefit limit.

- Life Insurance Net Cash Surrender & Net Cash Withdrawal Values: California covers 80% of the cash surrender value with a $100,000 benefit limit.

- Other Health Insurance Benefits: California’s health insurance benefit protection has increased from the January 1, 1991, statutory amount of $200,000 based on changes in the health-care cost component of the Consumer Price Index and is locked in for a particular insolvency on the date of liquidation. As of June 30, 2024, the amount of benefit protection for health insurance was $668,205. Benefit protection for an insolvency occurring after June 30, 2024, could increase or decrease depending on changes in the health-care cost component of the Consumer Price Index.

- Annuities: California covers 80% of the annuity contract value with a $250,000 benefit limit.

Colorado

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Connecticut

$500,000

Life Insurance Death Benefits

$500,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$500,000

Annuities

Delaware

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

District of Columbia

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$300,000

Annuities

Florida

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$250,000

Annuities

Notes

- Annuities: The $250,000 benefit limit applies if the annuity is deferred. If the annuity is in payout status, a $300,000 limit applies.

Georgia

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$250,000

Annuities

Notes

- Annuities: The $250,000 benefit limit applies if the annuity is deferred. If the annuity is in payout status, a $300,000 limit applies.

Hawaii

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Idaho

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$250,000

Annuities

Illinois

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Indiana

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Iowa

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Kansas

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Kentucky

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Louisiana

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$250,000

Annuities

Maine

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$250,000

Annuities

Maryland

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Massachusetts

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Michigan

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Minnesota

$500,000

Life Insurance Death Benefits

$130,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$410,000

Annuities

Notes

- Annuities: In Minnesota, the benefit is $410,000 for structured settlements and for annuities that have been annuitized for not less than lifetime or for a period certain not less than 10 years.

Mississippi

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Missouri

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Montana

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Nebraska

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Nevada

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

New Hampshire

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

New Jersey

$500,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$No limit

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$No limit

Long-Term Care & Disability Income Insurance Benefits

$No limit

Other Health Insurance Benefits

$250,000

Annuities

Notes

- Other Health Insurance Benefits: New Jersey sets no dollar cap on its medical coverage, covering claims up to the limits of the policy but limiting the benefit to 80% if the provider seeks coverage as opposed to the insured.

- Annuities: In New Jersey, if the annuity is in payout status with no cash surrender value, the limit is $500,000 in present value. The $250,000 benefit limit applies to deferred annuities.

New Mexico

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

New York

$500,000

Life Insurance Death Benefits

$500,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$500,000

Annuities

North Carolina

$300,000

Life Insurance Death Benefits

$300,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$300,000

Annuities

Notes

- Annuities: North Carolina applies a $300,000 annuity limit except for structured settlement annuities (SSAs), for which the limit is $1 million, and unallocated annuities owned as part of a specific benefit plan or in connection with government lotteries, for which the limit is $5 million.

North Dakota

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Ohio

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Oklahoma

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$300,000

Annuities

Oregon

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Pennsylvania

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Rhode Island

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

South Carolina

$300,000

Life Insurance Death Benefits

$300,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$300,000

Annuities

South Dakota

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Tennessee

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Texas

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$200,000

Other Health Insurance Benefits

$250,000

Annuities

Utah

$500,000

Life Insurance Death Benefits

$200,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$500,000

Annuities

Notes

- Life Insurance Death Benefits: In Utah, the $500,000 limit applies if death occurs before the guaranty association is triggered. If death occurs after triggering, the benefit is limited to the covered portion of the policy as defined by statutory reference to the covered cash value.

Vermont

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Virginia

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Washington

$500,000

Life Insurance Death Benefits

$500,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$500,000

Long-Term Care & Disability Income Insurance Benefits

$500,000

Other Health Insurance Benefits

$500,000

Annuities

West Virginia

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Wisconsin

$300,000

Life Insurance Death Benefits

$300,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$500,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$300,000

Other Health Insurance Benefits

$300,000

Annuities

Wyoming

$300,000

Life Insurance Death Benefits

$100,000

Life Insurance Net Cash Surrender & Net Cash Withdrawal Values

$300,000

Basic Hospital, Medical & Surgical Insurance or Major Medical Insurance Benefits

$300,000

Long-Term Care & Disability Income Insurance Benefits

$100,000

Other Health Insurance Benefits

$250,000

Annuities

Continuing Your Coverage

When an insurance company fails, policyholders often worry about losing their coverage—especially if they purchased their life or health insurance policy years or even decades ago. Fortunately, in addition to paying claims, the life and health insurance safety net also includes a crucial feature: continuing coverage.

If your policy gives you the right to continue coverage, you can do so—even if your company fails. Guaranty associations honor the terms of your policy (up to the benefit limits mentioned above) as if the insurance company were still in business. They do this by either:

Transferring Policies

Guaranty associations sometimes transfer policies—even those for people who might now be uninsurable—from the insolvent company to a financially stable insurer.

Paying Claims

In some cases, guaranty associations manage the policies and pay claims themselves.

In either case, you’ll still have coverage through the safety net provided by the guaranty associations.

© 2001-2026 All Rights Reserved | Terms Of Use | Site Help